Wall Street experienced a remarkable rebound on Thursday, with the S&P 500 enjoying its best day since November 2022. This surge followed new labour market data that boosted investor confidence in the US economy, recovering from a sharp sell-off earlier in the week. Major indices, including the Dow Jones Industrial Average and the Nasdaq Composite, posted substantial gains, driven by strong performances in technology and pharmaceutical stocks. The positive jobless claims figures signalled resilience in the labour market, further uplifting market sentiment and fuelling the broad recovery.

Key Takeaways:

- S&P 500 Achieves Best Day Since 2022: The S&P 500 surged 2.3%, closing at 5,319.31, marking its best performance since November 2022. This remarkable gain follows a sharp market sell-off earlier in the week and demonstrates a robust recovery, boosted by positive labour market data which reassured investors about the resilience of the US economy.

- Dow Jones Industrial Average Sees Strong Gains: The Dow Jones Industrial Average experienced a substantial increase, rising 683.04 points, or 1.76%, to close at 39,446.49. This strong performance highlights the broad recovery across major stock indices and reflects investor optimism following encouraging economic indicators.

- Nasdaq Composite Rallies Amid Tech Resurgence: The Nasdaq Composite climbed 2.87%, ending the session at 16,660.02. The index was driven by strong performances in the technology sector, with chipmakers Nvidia and Broadcom both jumping by more than 6%. Additionally, Meta Platforms climbed 4.2%, and Apple ticked up about 1.7%, showcasing renewed investor confidence in tech stocks.

- Labour Market Data Boosts Sentiment: Weekly jobless claims came in at 233,000, down 17,000 from the previous week and below the Dow Jones estimate for 240,000. Despite rising continuing claims, which reached 1.875 million—the highest since November 2021—the reduction in initial jobless claims helped to allay fears.

- 10-Year Treasury Yield Climbs: US Treasury yields rose on Thursday as Wall Street responded to the positive weekly jobless claims data, which eased concerns from the previous week’s disappointing payroll report. The yield on the 10-year Treasury increased by approximately 3 basis points, reaching 3.992%, nearing its highest level since last Thursday. Similarly, the 2-year note yield climbed nearly 4 basis points to 4.036%.

- Airline Stocks Outperform: Airline stocks showed strong performance during Thursday’s market rally, indicating increased investor confidence in the state of the economy. The US Global Jets ETF (JETS) was up about 3% in afternoon trading, with American Airlines and Delta Air Lines each gaining more than 4%, contributing to the ETF’s overall gains.

- European Markets Close Mixed: European stocks closed slightly higher, with the pan-European Stoxx 600 index up 0.02% after spending most of the session in the red. Sectors showed mixed performance, with travel stocks gaining 1.28%, while media and chemicals stocks both slipped 0.6%. The FTSE 100 Index fell by 0.27% to 8,144.97, and the CAC 40 dipped 0.3% to close at 7,191, weighed down by losses in heavyweight companies such as L’Oréal and Airbus.

- Asia Markets React to Global Data: Asian markets experienced mixed performance amid global economic data and investor sentiment. Japan’s Nikkei 225 dipped 0.74% to end at 34,831.15, while the Topix dropped 1.11% to 2,461.7. Mainland China’s CSI 300 reversed earlier losses to end roughly flat at 3,342.94, and Hong Kong’s Hang Seng index rose 1.3% to 16,866.51, reflecting cautious optimism.

- Oil Prices Rise Amid Positive Labour Data and Middle East Tensions: US crude oil futures climbed over 1% on Thursday, surpassing $76 per barrel as encouraging labour market data eased recession worries and ongoing Middle East tensions provided additional support. West Texas Intermediate (WTI) crude rebounded strongly, closing at $76.19 per barrel, up 1.28%, lifted by the sixth consecutive week of falling crude inventories. Brent crude futures closed up 1.06% to $79.16 a barrel. The market remains vigilant over the possibility of Iran retaliating against Israel. Brent crude for October delivery also saw gains, ending at $79.16 per barrel, up 1.06%. Year to date, US crude has risen by 6.34%, while Brent has increased by 2.75%.

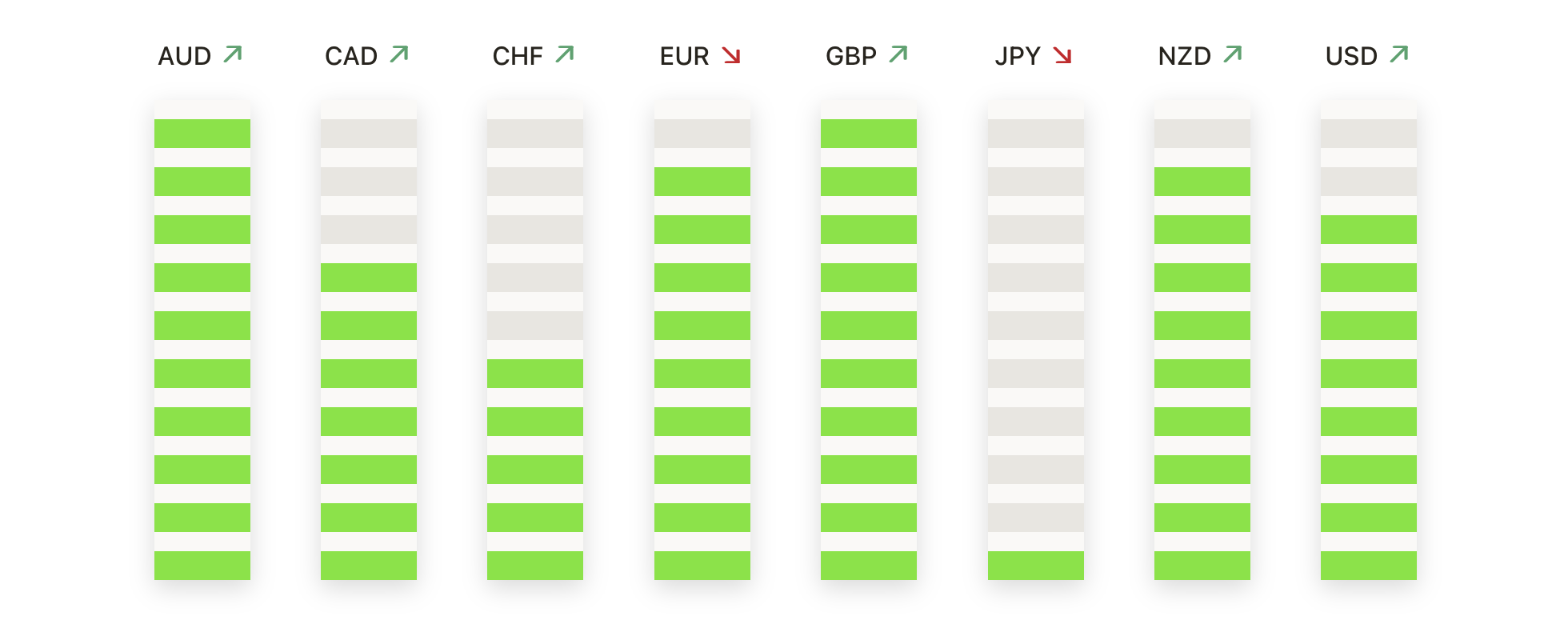

FX Today:

- Gold Prices Climb Amid High US Yields: Gold prices climbed during the North American session on Thursday, with XAU/USD trading at $2,423, up over 1.70%. This rally came despite a stronger US Dollar and rising US yields. The precious metal brushed aside these factors, reaching new weekly highs of $2,424. Buyers are now eyeing the psychological $2,450 level. If prices push above $2,450, the next targets are $2,477 and the all-time high of $2,483. Conversely, a drop below $2,368 could lead to further declines to $2,346 and support around $2,316, with $2,300 as a key support level.

- GBP/USD Rebounds Around 200-DMA, Climbs Above 1.2700: The Pound Sterling made a significant rebound during the North American session, trading at 1.2745, up over 0.40%. This surge occurred after the pair neared the 200-day moving average (DMA) at 1.2654. For a bullish continuation, buyers need to reclaim the 50-DMA at 1.2785, followed by the 1.2800 figure. The next targets would be at 1.2888 and the 1.2900 mark. On the downside, if sellers drag the exchange rate below 1.2700, it could test at 1.2683 and 1.2654.

- Australian Dollar Gets a Boost Due to Hawkish RBA Signs: The AUD/USD pair recorded an upturn at 0.6590 during Thursday’s sessions, rising notably by 1.10%. This increase was driven by the Reserve Bank of Australia’s (RBA) recent hawkish signals and rising commodity prices. The AUD/USD has been trading within a range between support at 0.6350 and resistance at 0.6590. The Relative Strength Index (RSI) rose toward 40, indicating a recovery in bullish sentiment and a balance between buying and selling pressures.

- Canadian Dollar Follows Market Flows on Thursday: The Canadian Dollar found some strength against the US Dollar, with USD/CAD trading near the 50-day Exponential Moving Average (EMA) at 1.3731. The pair is down 1.58% from last week’s peak above 1.3900. Long-term traders are watching for a continued easing toward the 200-day EMA at 1.3623. The immediate chart scenario indicates a technical bounce from the divergence zone between the 50-day and 200-day EMAs.

- USD/JPY Maintains Upward Momentum: The USD/JPY pair reclaimed the area beyond the 147.00 mark amid a broad-based risk-on mood, a stronger US Dollar, and higher US yields across the curve. The pair registered its largest gains since March 2023, influenced by comments from BoJ officials. If USD/JPY extends its gains past 148.00, it could test 148.45, with further targets at 149.00 and 151.50. On the downside, support levels are at 146.37, 146.00, and 145.00, with additional support at the August low of 143.61.

- EUR/USD Faced Additional Selling Pressure: The pair revisited sub-1.0900 levels. The pair’s negative price action was driven by the ongoing recovery of the US Dollar (USD) and positive sentiment in global stock markets. EUR/USD is likely to test the August high of 1.1008, with further resistance at the December 2023 top of 1.1139. On the downside, the pair’s next objectives are the 200-day SMA at 1.0832, the weekly low of 1.0777, and the June low of 1.0666, preceding the May low of 1.0649. The pair’s positive bias should hold if it trades above the crucial 200-day SMA.

Market Movers:

- Eli Lilly Surges on Strong Earnings: Pharmaceutical giant Eli Lilly saw its stock jump 9.5% after posting better-than-expected earnings and raising its full-year outlook. Strong demand for its diabetes treatment Mounjaro and obesity drug Zepbound drove the company’s impressive performance.

- Under Armour Pops on Quarterly Beat: Shares of Under Armour soared 19% after the athletic apparel maker topped quarterly estimates and adjusted its full-year profit guidance. The company’s strong results reassured investors of its growth trajectory.

- Warner Bros. Discovery Declines on Impairment Charge: Warner Bros. Discovery shares dropped 9% after the media company reported a $9.1 billion non-cash impairment charge on its TV networks business. The company also posted a wider-than-expected loss and missed revenue expectations.

- Occidental Petroleum Jumps on Earnings Beat: Shares of Occidental Petroleum rose 4.3% following the company’s quarterly results that exceeded analyst expectations. The firm benefited from higher oil production in Colorado and a rise in crude prices.

- Klaviyo Shares Skyrocket on Earnings: Klaviyo shares surged more than 33% after the marketing platform provider surpassed Wall Street’s top-and-bottom-line expectations, posting earnings of 15 cents per share and $222 million in revenue.

- Zillow Rallies on Strong Earnings: Zillow shares jumped more than 18% after the real estate platform reported second-quarter earnings that exceeded analyst estimates. The company posted adjusted earnings of 39 cents per share on $572 million in revenue.

- SolarEdge Technologies Falls on Wider Loss: SolarEdge Technologies shares tumbled 3% after the company reported an adjusted loss of $1.79 per share for the second quarter, wider than the expected loss of $1.58 per share. However, quarterly revenue of $265 million topped the $262 million consensus estimate.

- JFrog Plummets on Weak Guidance: JFrog shares plunged 27.5% after issuing light third-quarter guidance, expecting earnings to range between 9 and 11 cents per share versus an estimate of 14 cents.

As the market rebounds from Monday’s sell-off, the S&P 500’s best day since 2022 highlights the renewed investor confidence driven by positive labour market data and strong performances from major companies. With significant gains in tech and pharmaceutical stocks, alongside the encouraging jobless claims report, investors are hopeful. However, mixed signals from global markets and ongoing geopolitical tensions continue to underscore the complexity of the economic landscape. As the week progresses, market participants remain vigilant, balancing optimism with prudence, and closely monitoring economic indicators for further direction.