In a strong rebound from recent losses, the Dow Jones Industrial Average surged nearly 300 points on Tuesday, breaking a three-day losing streak. Investors showed renewed confidence as they took a pause from recession fears, with major indices like the S&P 500 and Nasdaq Composite also posting significant gains. The rally was driven by a broad market uplift, particularly in tech stocks, and was boosted by a historic surge in Japanese equities. Despite the backdrop of global economic uncertainties, including volatile carry trades and fluctuating crude oil prices, market sentiment turned positive, reflecting optimism about the resilience of key economic indicators and corporate earnings.

Key Takeaways:

- Dow Snaps Three-Day Losing Streak: The Dow Jones Industrial Average rose 294.39 points, or 0.76%, to close at 38,997.66, ending a three-day losing streak. This rally reflects a temporary pause in recession fears among investors. The broader market saw a wave of relief as concerns over economic instability and volatility began to subside, at least momentarily.

- S&P 500 and Nasdaq Composite Surge: The S&P 500 advanced 1.04%, closing at 5,240.03, while the tech-heavy Nasdaq Composite gained 1.03% to finish at 16,366.85. Both indices recovered from significant losses in the previous sessions. This broad-based recovery highlights investor optimism and resilience, particularly in the technology sector, which had faced sharp pullbacks earlier.

- Japanese and Asian Markets Post Historic Gains: Japan’s Nikkei 225 surged 10.23% to close at 34,675.46, marking its best day since October 2008 and the largest single-day points gain in its history. This remarkable recovery comes after a drastic 12.4% drop in the previous session, the worst since the 1987 Black Monday crash. Other Asia-Pacific markets also showed strength, with South Korea’s Kospi jumping 3.3% and the Kosdaq rising 6.02%. Mainland China’s CSI 300 and Hong Kong’s Hang Seng Index remained relatively stable, reflecting a mixed but generally positive regional response.

- European Markets Recover Slightly: The pan-European Stoxx 600 closed up 0.2%, bouncing back after losing over 2% in each of the previous two sessions. The UK’s FTSE 100 rose 0.23%, supported by gains in technology stocks. However, France’s CAC 40 and Germany’s DAX dipped slightly by 0.27% and 0.1%, respectively. The fluctuation in European markets underscores ongoing investor caution amid global economic uncertainties.

- Oil Prices and Saudi Aramco’s Earnings: US crude oil rose above $73 a barrel, with the West Texas Intermediate closing at $73.20 per barrel, up 0.36%. Brent crude increased to $76.48 per barrel, up 0.24%. These price movements come as the market braces for potential geopolitical impacts from escalating tensions between Iran and Israel. Concurrently, Saudi Aramco reported a second-quarter net profit of $29.1 billion, a slight dip of just over 3% from the same period last year due to lower crude production volumes.

- Treasury Yields Rebound: The yield on the 10-year Treasury note climbed 11 basis points to 3.901%, recovering from its lowest level in more than a year. The 2-year Treasury yield also rose, adding 10 basis points to 3.981%. These increases reflect investor confidence returning to the bond market, reversing the previous day’s sharp declines caused by global market sell-offs. The rebound in yields indicates a shift in market sentiment, with investors cautiously optimistic about the stability of the financial system.

FX Today:

- Yellow Metal Retreats as Bond Yields Surge: Gold prices fell below $2,400, influenced by increasing US yields and a strong USD, shifting market momentum sharply bearish. If XAU/USD dips below $2,365, further declines to $2,340 and support around $2,315 are possible. Breaching these levels may see prices head towards $2,300. On the upside, a recovery above $2,400 could target resistance at $2,450, followed by $2,477 and the all-time high of $2,483.

- GBP/USD Hits Multi-Week Dip Amid Selling Pressure: The GBP/USD pair tested at 1.2683 and hit a five-week low of 1.2672 before buyers lifted it to around 1.2700. The path of least resistance remains downward, with support at 1.2700, 1.2683, 1.2648. Further weakness could challenge 1.2600. Conversely, climbing above 1.2783 might spark a rally past 1.2800, targeting 1.2900.

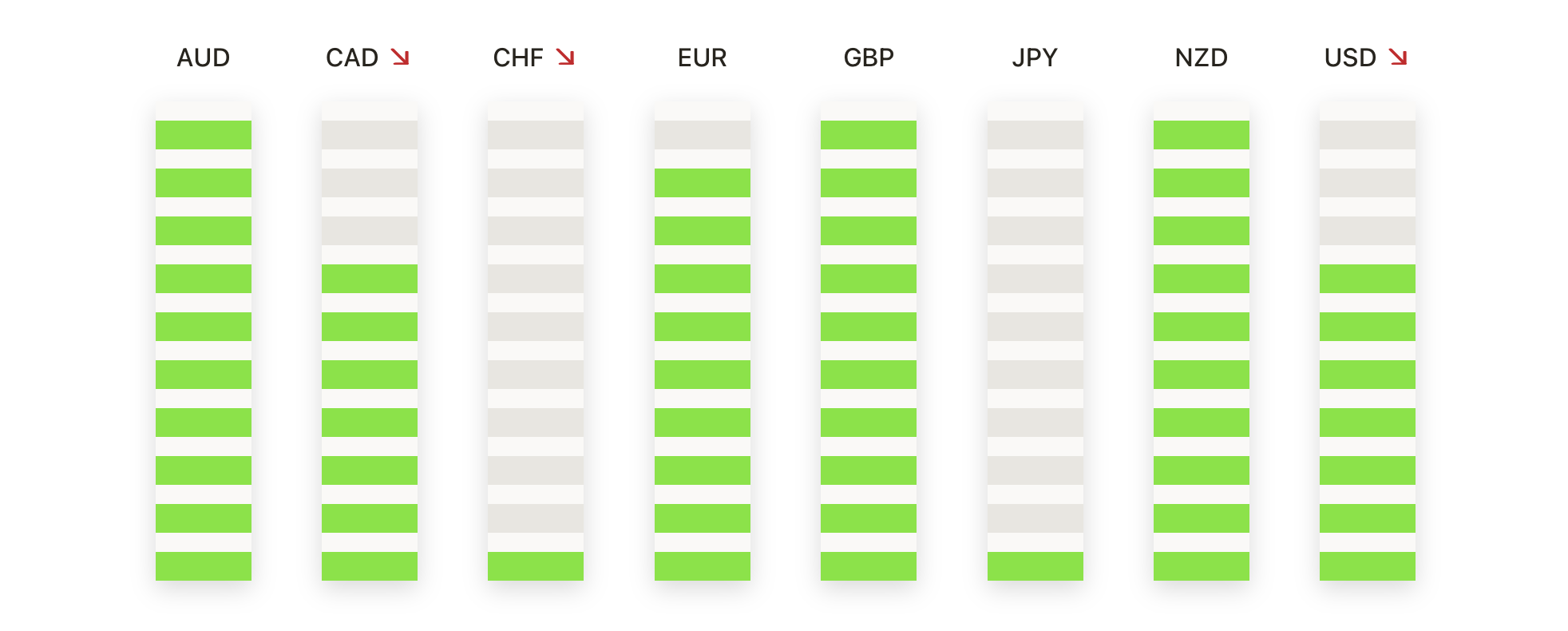

- CAD Mixed Performance Reflects Market Sentiment: The Canadian Dollar (CAD) rose 0.9% against the struggling Pound Sterling but eased 0.2% against the day’s strongest currency, the Japanese Yen. Against the US Dollar, CAD gained 0.2%, with USD/CAD slipping below 1.3800 from its recent peak near 1.3950. Despite the pullback, bearish momentum has not yet driven the pair below 1.3730, indicating potential consolidation.

- EUR/GBP Advances to New Highs on Pound Weakness: EUR/GBP climbed above 0.8600 for the second day, as the BoE’s interest rate cut to 5.0% led to outflows from GBP. The pair is poised to break past at 0.8545, targeting the 0.8650 level last seen in January. This marks the fourth consecutive daily gain for the pair, highlighting strong euro performance amid shifting market dynamics.

- AUD/JPY Maintains Bearish Outlook Despite Gains: AUD/JPY rose by 1.20% to 94.70, recovering some recent losses. However, it remains in a bearish consolidation phase, trading below the 20, 100, and 200-day SMAs. A decline below 94.60 could lead to further drops towards 94.00. Resistance lies between 94.50 and 95.50, and breaking above this range may improve the negative outlook, though bears remain in control.

- US Dollar Strengthens Ahead of Fed Decisions: The US Dollar (USD), tracked by the DXY Index, approached 103.00 on improved market sentiment. Despite recent RSI declines into oversold territory, a slight recovery was observed on Tuesday. The DXY remains bearish below the 20, 100, and 200-day SMAs. Key supports are at 102.50, 102.30, and 102.00, while resistances are at 103.00, 103.50, and 104.00, as markets anticipate future Federal Reserve decisions.

Market Movers:

- Airbnb Shares Plunge After Earnings Miss and Demand Warning: Airbnb shares dropped 16% in after-hours trading after the company reported second-quarter earnings that missed analyst expectations. Additionally, the company warned of slowing demand from US customers, further contributing to the stock’s decline.

- Kenvue Rallies on Earnings Beat: Kenvue, the maker of Band-Aid bandages, surged 14.68% after reporting second-quarter adjusted earnings of 32 cents per share, beating analysts’ expectations of 28 cents. Revenue came in at $4 billion, surpassing the consensus estimate of $3.93 billion, highlighting strong performance since its spinoff from Johnson & Johnson.

- Palantir Technologies Jumps on Upgraded Forecast: Shares of Palantir Technologies rose 10.38% after the defence tech company raised its full-year revenue forecast. The new guidance projects revenue between $2.742 billion and $2.750 billion, up from the previous range of $2.68 billion to $2.69 billion, reflecting strong demand for its AI-driven solutions.

- Lumen Technologies Soars on AI-Fuelled Demand: Lumen Technologies’ stock skyrocketed by 93.05% after announcing $5 billion in new business driven by increased demand for AI-powered connectivity solutions. This substantial gain reflects the market’s positive response to Lumen’s growth prospects in the rapidly expanding AI sector.

- Uber Technologies Up on Positive Earnings Report: Uber Technologies’ stock increased by 10.93% following its earnings report, which beat expectations. The company posted second-quarter earnings of 47 cents per share, outpacing the anticipated 31 cents per share, with revenue at $10.7 billion, higher than the $10.57 billion consensus estimate. This growth highlights Uber’s strong market position and expanding user base.

- Yum China Advances on Earnings Beat and Leadership Change: Yum China’s stock jumped 11.98% following its second-quarter earnings report, which beat expectations despite revenue coming in slightly below the consensus estimate. Additionally, the company announced the departure of its finance chief, signalling potential strategic shifts.

- ZoomInfo Technologies Falls on Disappointing Quarterly Report: Shares of ZoomInfo Technologies dropped 18.27% after the company reported lower-than-expected quarterly results. The firm earned an adjusted 17 cents per share on $291.5 million in revenue, missing the 23 cents per share on $308 million expected by analysts. ZoomInfo also revised its full-year earnings guidance downward and announced a change in its chief financial officer.

- CSX Gains on Solid Quarterly Earnings: CSX shares rose nearly 4% following the rail transportation company’s second-quarter earnings report. CSX posted earnings of 49 cents per share, slightly above the 48 cents expected by analysts. Revenue matched the consensus estimate at $3.7 billion, reflecting stable operational performance.

- CrowdStrike Rises on Analyst Upgrade: Shares of CrowdStrike rose 4.34% after Piper Sandler upgraded the cybersecurity company to overweight from neutral. The analyst cited the recent dip in CrowdStrike’s stock following a global tech outage as a buying opportunity. Despite a 10% decline this year, the stock has fallen 40% this quarter, suggesting potential for a rebound.

As markets continue to navigate through volatility and investor sentiment fluctuations, today’s broad relief rally indicates a temporary pause in recession fears, with notable recoveries in key indices and sectors. The Dow’s nearly 300-point rise and significant gains in the S&P 500 and Nasdaq Composite highlight a renewed optimism, especially in tech stocks and amid the impressive rebound in Japanese equities. Meanwhile, fluctuating oil prices and mixed performances in individual stocks underscore the complexities of current economic conditions. As the week progresses, investors will closely monitor further economic indicators and corporate earnings reports for signs of sustained stability or emerging risks.