Stocks closed lower on Wednesday in a volatile session marked by the Federal Reserve’s aggressive half-point interest rate cut and new inflation data from the UK and Eurozone. While the Fed’s decision initially lifted markets, concerns quickly emerged that the central bank might be pre-emptively responding to potential economic weakness. European markets faced additional pressure amid stagnant inflation figures, and Asian markets displayed mixed performances. Investors faced with a slew of data, including surging mortgage demand in the US, fluctuating oil prices, and significant movements in the foreign exchange markets.

Key Takeaways:

- Dow Drops Over 100 Points Despite Early Gains: The Dow Jones Industrial Average fell 103.08 points or 0.25%, closing at 41,503.10. The index was up as much as 375.79 points immediately after the Fed’s announcement but failed to maintain momentum due to rising investor concerns.

- S&P 500 and Nasdaq Retreat After Touching Records: The S&P 500 lost 0.29% to end at 5,618.26, and the Nasdaq Composite dropped 0.31% to 17,573.30. Both indices reached record highs earlier in the session before reversing course.

- Federal Reserve Cuts Rates to 4.75%-5%: In its first rate cut in four years, the Fed lowered the overnight lending rate by 50 basis points to a range of 4.75%-5% from 5.25%-5.5%. The move was larger than the traditional quarter-point adjustments, signalling a proactive stance against potential economic headwinds.

- Mortgage Demand Surges as Rates Hit Two-Year Low: Total mortgage application volume in the US rose 14.2% last week, according to the Mortgage Bankers Association. The average contract interest rate for 30-year fixed-rate mortgages decreased to 6.15% from 6.29%, the lowest since September 2022, spurring increased borrowing activity.

- European Markets Close Lower Amid Inflation Concerns: The pan-European Stoxx 600 index declined 0.49%. The FTSE 100 dropped 0.68% to 8,253.68, marking a decline of 56.18 points. France’s CAC 40 fell 0.57%, and Germany’s DAX closed slightly below the flatline at 18,711. UK inflation held steady at 2.2% in August, matching expectations but indicating stagnant price growth. Core inflation in the UK rose to 3.6% from 3.3%, potentially adding pressure on the Bank of England ahead of its rate decision. The Eurozone’s annual inflation was confirmed at 2.2% in August, down from 2.6% in July, while core inflation edged down to 2.8% from 2.9%.

- Asian Markets Mixed Amid Fed Anticipation and Economic Data: Japan’s Nikkei 225 rose 0.49% to 36,380.17, and the Topix added 0.38% to 2,565.37, despite weaker-than-expected machinery orders and trade data. Australia’s S&P/ASX 200 edged up marginally to close at an all-time high of 8,142.1, extending its winning streak. Mainland China’s CSI 300 increased 0.37% to 3,171, while Taiwan’s Weighted Index fell 0.78% to 21,850.08. South Korea and Hong Kong markets were closed for a holiday. Investors across the region were cautious ahead of the Fed’s rate decision and assessed domestic economic indicators.

- Oil Prices Edge Lower Despite Fed Rate Cut: West Texas Intermediate (WTI) crude settled at $70.91 per barrel, down $0.28 or 0.39%. Brent crude closed at $73.65 per barrel, a decrease of $0.05 or 0.07%. The oil market’s muted response reflects ongoing concerns about a potential supply-demand imbalance, slowing consumption in China, and increased production from OPEC+ members and other countries.

- Treasury Yields Rise Post-Fed Decision: The yield on the 10-year Treasury note increased by 6 basis points to 3.713%, while the 2-year Treasury yield added over 2 basis points to 3.628%. The rise suggests that investors remain wary of long-term inflation risks despite the Fed’s rate cut.

FX Today:

- Gold Pulls Back After Hitting Record High Post Fed Cut: Gold prices eased after reaching an all-time high on Wednesday, following the US Federal Reserve’s half-percentage-point interest rate cut. The precious metal faced rejection after attempting to break above the $2,600 mark, pulling back to trade near $2,558.90. The price is approaching the 50-period SMA around $2,542.83, which may serve as initial support for bullish traders. A failure to hold above this level could see gold targeting the 100-period SMA near $2,524.51, with the 200-period SMA at $2,493.18 acting as key support in case of further decline. On the upside, a rebound could lead to a renewed push toward the $2,600 psychological resistance, with a successful break potentially signalling a continuation of the bullish trend.

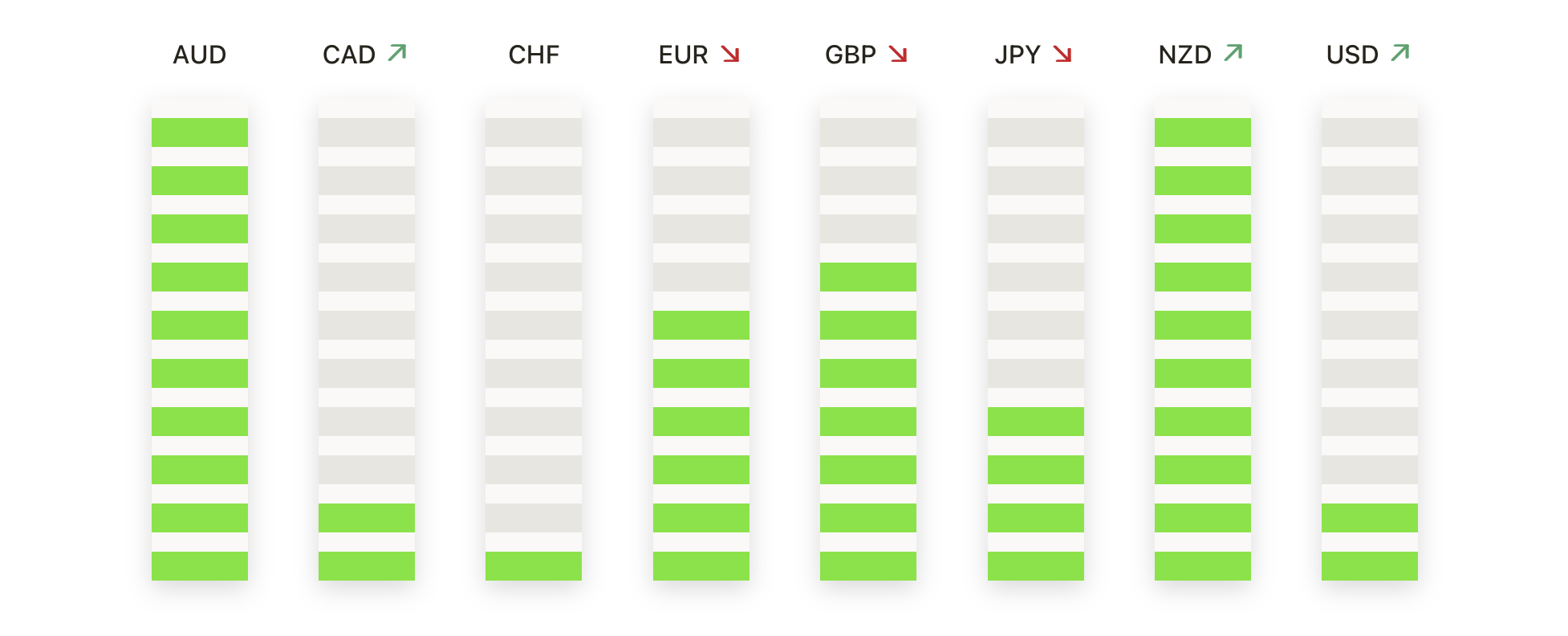

- Euro Holds Steady Amid Fed Rate Cut and Inflation Data: EUR/USD has entered a consolidation phase, trading around 1.1118 after failing to decisively break above the 1.1150 resistance level. The pair remains above the 50-period and 100-period SMAs, indicating that the broader bullish trend remains intact. Multiple attempts to push above 1.1150 have faced strong selling pressure, suggesting a breakout is needed for further upside potential. If resistance holds, a pullback toward the 50-period SMA around 1.1070 is possible, with additional support at the 200-period SMA near 1.1049. A break above 1.1150 could see the pair targeting the 1.1200 mark.

- British Pound Extends Gains, Targets Higher Resistance: GBP/USD continues to maintain its bullish momentum, trading near 1.3212 as the pair pushes higher after finding support at the 50-period SMA. The price action remains above both the 50-period and 100-period SMAs, providing strong bullish signals. Immediate resistance lies near 1.3250, with potential further gains if the price breaks above this level. On the downside, failure to maintain momentum could see a pullback toward the 200-period SMA around 1.3140, acting as key support. As long as the price stays above this level, the bullish trend remains intact, with traders eyeing a possible move toward 1.3300.

- Australian Dollar Nears Breakout Point Amid USD Weakness: AUD/USD is trading around 0.6765, hovering near key resistance levels after a strong recovery. The pair has found support around the 50-period and 100-period SMAs, which are converging near the 0.6730 level. Bulls are trying to maintain momentum, but resistance near 0.6800 has so far prevented a sustained breakout. A successful move above this resistance could lead to further gains toward the 0.6850 level. On the downside, any weakness could see the pair retesting the 200-period SMA near 0.6683, which has provided solid support in recent price action. Traders are closely watching for a breakout or breakdown from current levels to determine the next direction.

- Japanese Yen Experiences Sharp Swings After Fed Decision: USD/JPY plunged to 140.80 on Wednesday after the Federal Reserve delivered a 50 bps rate cut but quickly recovered to trade near 142.40. The pair is now trading within a familiar technical zone, threatening a consolidation trap that could squeeze both buyers and sellers in a tight but volatile range. Key support levels are at 140.89, 139.53, and 138.62, while resistance levels are noted at 143.16, 144.07, and 145.43. Market participants remain cautious amid the sharp fluctuations, with attention on upcoming economic data and central bank commentary.

Market Movers:

- Intuitive Machines Soars on NASA Contract: Shares of Intuitive Machines surged 38.3% after securing a roughly $5 billion space network contract from NASA, significantly boosting investor confidence in the company’s long-term prospects.

- United States Steel Gains Amid Acquisition Developments: United States Steel shares rose 1.5% following news that a US security panel has granted Nippon Steel permission to refile its $14.1 billion acquisition plans. The move could delay a decision until after the November presidential election, providing additional time for regulatory review.

- Victoria’s Secret Upgraded, Shares Advance: Victoria’s Secret shares increased 3.5% after Barclays upgraded the stock to “equal weight” from “underweight,” citing a more balanced risk/reward profile. The bank now sees more than 6% upside potential for the stock.

- VF Corporation Climbs on Analyst Upgrade: VF Corporation shares climbed 3.9% after Barclays upgraded the company to “overweight” from “equal weight,” anticipating that benefits from last year’s CEO change will begin to materialise this fall.

- Medical Properties Trust Declines on Impairment News: Shares of Medical Properties Trust dropped 4.8% after the company announced an anticipated additional impairment of about $430 million in Q3, following a settlement with tenant Steward, which filed for Chapter 11 bankruptcy.

- ResMed Shares Drop on Revenue Growth Concerns: ResMed shares shed 5.1% after Wolfe Research downgraded the stock to “underperform” from “peer perform,” citing anticipated deceleration in revenue growth due to increased competition from Eli Lilly’s GLP-1 medication.

- Casella Waste Systems Declines on Stock Offering Announcement: Casella Waste Systems shares fell 5.8% after announcing a $400 million public offering of its Class A common stock, raising dilution concerns among existing shareholders.

Financial markets navigated a complex array of economic data and policy decisions on Wednesday. The Federal Reserve’s unexpected half-point rate cut initially lifted investor sentiment but eventually led to concerns about potential economic slowdown, causing declines in major US indices. European markets were pressured by stagnant inflation figures in the UK and Eurozone, raising questions about future monetary policy moves by the Bank of England and the European Central Bank. Asian markets presented a mixed picture amid varying regional data and anticipation of the Fed’s decision. The surge in US mortgage demand highlighted the immediate impact of lower interest rates on consumer activity. In commodities, oil prices edged lower despite the rate cut, reflecting ongoing supply and demand uncertainties. Currency markets experienced significant volatility, particularly among USD pairs, as traders adjusted positions in response to the Fed’s policy shift and regional economic indicators. With several central banks in focus this week, investors remain cautious, seeking clearer signals on the global economic outlook and the future trajectory of monetary policy.