Despite a day marked by anticipation for key economic data, US equity markets closed lower, reflecting investor caution ahead of a second-quarter GDP report and potential signals from the Federal Reserve on future rate cuts. The Nasdaq Composite, S&P 500, and Dow Jones Industrial Average all ended the day in negative territory, with tech stocks leading the declines. Meanwhile, European and Asia-Pacific markets showed mixed performances amid varying regional economic developments, including inflation data and corporate earnings. As global markets navigate these economic signals, investors are closely watching the unfolding economic narrative, balancing optimism with the challenges of a slowing growth environment.

Key Takeaways:

- Nasdaq Composite Falls Ahead of GDP Report: The Nasdaq Composite declined 1.12% to close at 17,556.03 as investors showed caution ahead of the upcoming second-quarter GDP report. Major technology stocks, including Amazon and Alphabet, each dropped more than 1%, contributing to the overall negative performance in the tech-heavy index.

- S&P 500 Slips Amid Economic Uncertainty: The S&P 500 slipped 0.6% to end at 5,592.18, reflecting broad market concerns about potential economic slowdown and the Federal Reserve’s policy outlook. The index faced headwinds from various sectors, particularly technology and consumer discretionary, as market participants remained cautious.

- Dow Jones Industrial Average Posts Modest Losses: The Dow Jones Industrial Average lost 159.08 points, or 0.39%, to settle at 41,091.42. Despite the modest loss, the Dow was relatively resilient compared to other US indices, with mixed performances across its constituent companies as investors await further economic data.

- European Markets Maintain Momentum: Despite the downturn in US markets, European stocks closed higher, with the pan-European Stoxx 600 up 0.33%. The gains were driven by strong performances in the chemicals sector, which rose 1.4%, and insurance stocks, up 1.16%. While the FTSE 100 Index remained almost unchanged, down only 1.61 points or 0.02% to 8,343.85, France’s CAC 40 edged up nearly 0.2% to close at 7,578. Economic data from France showed a slight increase in household confidence, adding to the positive sentiment in the region. Additionally, companies like British insurer Prudential reported a 9% jump in adjusted operating profit, briefly lifting shares by more than 2% before a pullback.

- Mixed Performance in Asia-Pacific Markets: The Asia-Pacific region saw varied results, with China’s CSI 300 index falling 0.57% to 3,286.5, reaching a near seven-month low, while Hong Kong’s Hang Seng index dropped 1.05%. The declines were influenced by higher-than-expected inflation figures in Australia, where the Consumer Price Index (CPI) rose 3.5% year on year, slightly above forecasts. In contrast, Japan’s Nikkei 225 rebounded from early losses to gain 0.22%, ending the day at 38,371.76, and the Topix index rose 0.42% to 2,692.12. South Korea’s Kospi ended flat at 2,689.83 while the Kosdaq slipped 0.32%, marking its sixth consecutive day of losses.

- US Mortgage Applications Rise Despite Lower Rates: Mortgage rates fell to their lowest since April 2023, with the average 30-year fixed-rate mortgage dropping to 6.44%. Despite the decline in rates, total mortgage application volume increased modestly by 0.5%, with purchase applications rising 1% week-over-week. However, refinancing demand decreased by 0.1%, as most borrowers already hold mortgages with rates significantly lower than the current average.

- Crude Oil Prices Decline Amid Weak Demand: US crude oil prices dropped more than 1% to settle at $74.61 per barrel, while Brent crude fell 0.99% to $78.76. The decline comes amid concerns over weak demand in China and risks of a broader economic slowdown, despite potential supply disruptions in Libya and ongoing geopolitical tensions in the Middle East.

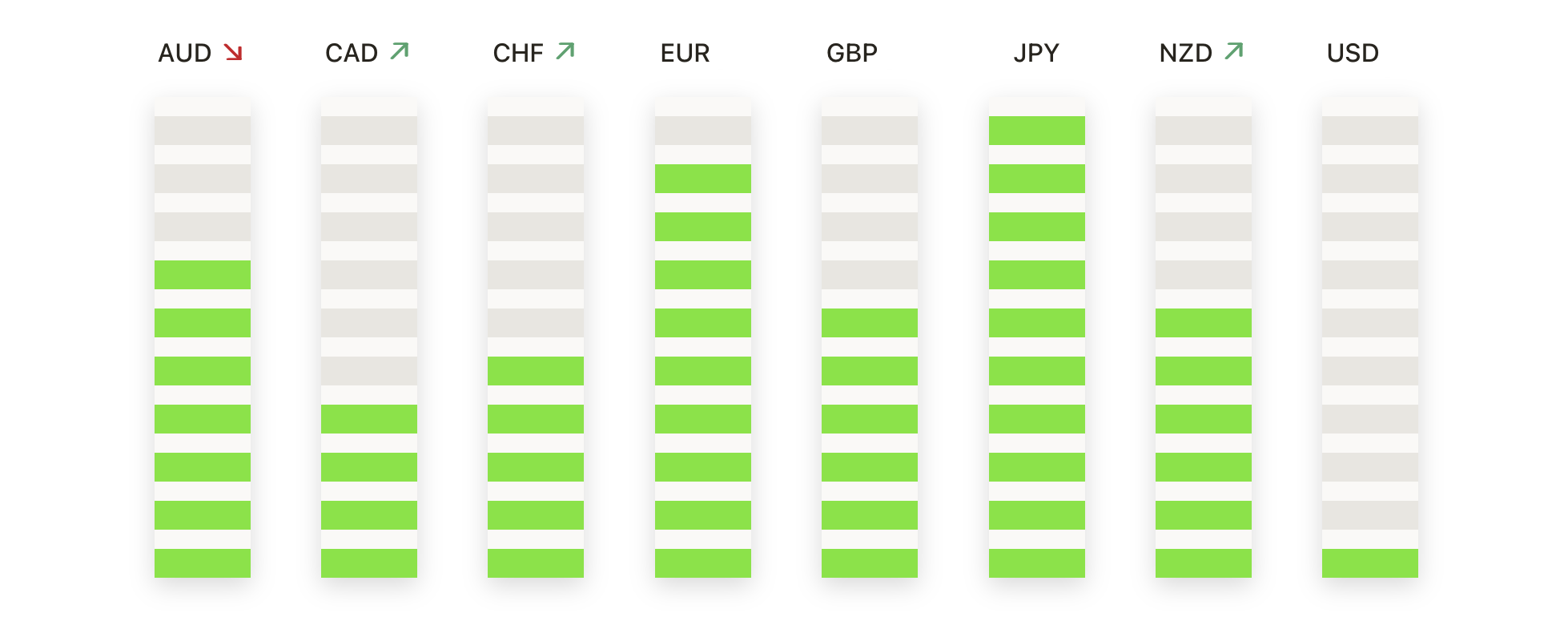

FX Today:

- EUR/USD Sinks as Market Eyes ECB Rate Cut: EUR/USD experienced a significant drop to around 1.1150 from its earlier high of 1.1200, losing 0.5% as the Euro weakened against the US Dollar. This movement reflects growing expectations of an ECB rate cut in September. The pair holds above key support at 1.1000 but may face further pressure if it continues downward. Upside potential remains if the Euro can reclaim ground towards resistance levels at 1.1275 and 1.1500.

- GBP/USD Retreats Below Key Level Amid Dollar Strength: The GBP/USD pair fell below the crucial 1.3200 level, trading around 1.3190, marking a 0.60% drop from its recent high of 1.3266. This decline comes as investors position themselves ahead of important US inflation data. Should the pair continue to weaken, support lies at 1.3044 and the 50-day moving average at 1.2857. If it can regain momentum above 1.3266, it might target resistance at 1.3299 and potentially climb towards 1.3400.

- USD/JPY Tests 145.00 Threshold on Renewed Dollar Demand: USD/JPY moved higher to 144.73, a recovery from earlier lows of 143.68, as the US Dollar regained strength, rising nearly 0.73%. The pair is approaching the critical 145.00 mark, a level that, if breached, could pave the way for further gains to 146.39 and 148.84. Failure to sustain this level could see the pair falling back towards support at 144.00, with further downside risk extending to 143.45 and 141.70.

- DXY Stabilises as Traders Await US Economic Clues: The US Dollar Index (DXY) held steady around 101.00, maintaining its position amid easing selling pressure. With support levels established at 100.50, 100.30, and 100.00, the index could see limited downside barring new economic data. Resistance is noted at 101.50 and 101.80, and market participants are looking forward to the upcoming US inflation report, which may set the stage for future moves.

Market Movers:

- Nvidia Drops Despite Beating Expectations: Nvidia shares fell 6% even after reporting fiscal second-quarter results that exceeded expectations. The company posted adjusted earnings per share of 68 cents, above the consensus estimate of 64 cents, and revenue of $30.04 billion, higher than the anticipated $28.7 billion. Despite the positive results, the market reaction was negative, possibly due to profit-taking.

- Salesforce Climbs on Strong Results and Guidance: Salesforce’s stock increased by 3.5% after the software giant reported better-than-expected fiscal second-quarter earnings and raised its full-year profit outlook. The company also announced that President and CFO Amy Weaver will step down, adding an element of leadership transition to its future outlook.

- Super Micro Computer Plummets After Postponing Filing: Shares of Super Micro Computer tumbled 19.1% after the company announced it would delay filing its annual 10-K form for the fiscal year that ended June 30. The decision came as the company’s management needs more time to assess the effectiveness of its internal controls over financial reporting. This news was compounded by Hindenburg Research revealing a short position in the stock, further pressuring shares.

- Neurocrine Biosciences Declines on Clinical Trial Concerns: Neurocrine Biosciences saw its shares drop by 19% following the release of top-line Phase 2 data for its schizophrenia drug. Despite reporting positive results, investors were concerned about the potential variability in outcomes for future trials. Stifel highlighted these concerns in a note, stating, “These data are clearly messier than hoped,” which added to the downward pressure on the stock.

- Abercrombie & Fitch Falls Amid Uncertain Outlook: Abercrombie & Fitch shares fell approximately 17% after CEO Fran Horowitz warned of an “increasingly uncertain environment” for the second half of 2024. Despite beating fiscal second-quarter expectations and raising its full-year sales outlook, the market focused on the cautious tone, driving the stock lower.

- Berkshire Hathaway Rises Nearly 1%, Reaches $1 Trillion Milestone: Berkshire Hathaway’s stock rose nearly 1%, crossing the $1 trillion market capitalization for the first time. This milestone makes it the first non-technology company in the US to reach this valuation, as shares have rallied 28% this year, significantly outperforming the S&P 500.

- HP Falls 4% on Disappointing Earnings: HP’s stock dipped 4% after the company reported fiscal third-quarter adjusted earnings of 83 cents per share, below the expected 86 cents per share. Although revenue came in at $13.52 billion, slightly above the consensus estimate of $13.38 billion, the earnings miss weighed on investor sentiment.

- Affirm Jumps 15% Following Upbeat Guidance: Shares of Affirm surged 15% after the buy now, pay later provider issued an optimistic forecast for its fiscal first-quarter revenue, projecting a range of $640 million to $670 million, above the analyst consensus of $625 million. Affirm also reported fiscal fourth-quarter results that exceeded Wall Street estimates, boosting investor confidence.

- Chewy Surges 11% Following Strong Earnings Beat: Chewy’s stock jumped around 11% after the pet retailer reported better-than-expected second-quarter results. The company posted an adjusted EBITDA of $144.8 million, significantly outperforming the analyst consensus of $111.7 million according to FactSet. This strong financial performance reinforced investor confidence in Chewy’s growth strategy.

As the market digests a mix of earnings results and macroeconomic signals, the latest movements across equities and currencies underscore a cautious yet reactive environment. With US equities broadly declining ahead of key GDP and inflation data, and mixed performances across global markets reflecting region-specific developments, investors are navigating a complex landscape. The Nasdaq’s drop, coupled with the S&P 500 and Dow Jones’s modest losses, highlights the current uncertainty and anticipation surrounding economic growth and potential policy shifts. Meanwhile, fluctuations in major currency pairs and ongoing concerns about inflation and labour market trends suggest a cautious approach as market participants await clearer indications from upcoming data and central bank actions.