US stocks made a strong comeback on Monday, with the Dow Jones Industrial Average soaring nearly 500 points, recovering from Wall Street’s worst week of 2024. Investors were optimistic, banking on a likely Federal Reserve rate cut later this month to provide a boost to the slowing economy. Technology stocks, which suffered most of last week’s selloff, led the recovery, with significant gains in retail, banking, and industrial shares adding to the rebound. Despite ongoing concerns about economic growth, markets were assured by the belief that the Fed’s next move could offer some much-needed relief.

Key Takeaways:

- Dow Jumps Nearly 500 Points After Worst Week of 2024: The Dow Jones Industrial Average surged 484.18 points, or 1.2%, to close at 40,829.59 on Monday. This rebound follows a significant drop of more than 1,200 points last week, as investors positioned themselves ahead of a likely Federal Reserve rate cut expected later this month to support the slowing US economy.

- S&P 500 and Nasdaq Break Losing Streaks with Over 1% Gains: The S&P 500 climbed 1.16%, finishing at 5,471.05, after posting its worst week since March 2023. Similarly, the Nasdaq Composite jumped 1.16% to close at 16,884.60, rebounding from its steepest weekly losses in over two years. These recoveries imply that these markets have shown resilience in the last week.

- European Markets Close Higher; FTSE 100 Up 1.09%: European markets began the week on a positive note. The pan-European Stoxx 600 index gained 0.76%, with travel and leisure stocks leading the charge, up 2.18%, and banking stocks adding 1.17%. The UK’s FTSE 100 rose 1.09% to 8,270.84. However, luxury stocks faced pressure, with Burberry shares falling 4.86% and France’s Kering down 2.48%. France’s CAC 40 index added 73 points, or 0.99%, led by gains in Air Liquide (+2.37%), Saint-Gobain (+2.13%), and Schneider Electric (+1.87%). Meanwhile, investors are now waiting for the ECB’s monetary policy decision on Thursday, where a 25 basis point rate cut is expected.

- Asian Markets Mixed Amid Economic Concerns: Asia-Pacific markets struggled on Monday, with Hong Kong’s Hang Seng Index leading the regional losses, down 1.77%. China’s CSI 300 fell 1.19% to 3,192.95, hitting a seven-month low as weaker-than-expected inflation data underscored concerns about the health of the Chinese economy. Japan’s Nikkei 225 declined 0.48%, closing at 36,215.75, while South Korea’s Kospi slipped 0.33% to 2,535.93. The Japanese yen weakened further, trading at 143.20 per US dollar, reflecting risk-off sentiment in the region. On the positive side, Australia’s S&P/ASX 200 outperformed, closing only slightly lower by 0.32% at 7,988.1.

- Oil Prices Rebound Over 1% After Worst Week Since 2023: US crude oil futures rebounded more than 1% on Monday, recovering from the worst week since October 2023. West Texas Intermediate (WTI) crude rose $0.97, or 1.43%, to settle at $68.65 per barrel, while Brent crude added $0.70, or 0.99%, to close at $71.76 per barrel. Both benchmarks have lost over 15% in the third quarter so far, reflecting broader concerns about global demand.

- Treasury Yields Steady Ahead of Key Inflation Data: US Treasury yields remained relatively unchanged as investors looked ahead to critical inflation reports due later this week. The yield on the 10-year Treasury held at 3.706%, while the 2-year Treasury yield rose by 3 basis points to 3.681%. Markets remain focused on the Federal Reserve’s next rate decision, with expectations building for a potential cut that could ease pressure on borrowing costs and offer support to the flagging economy.

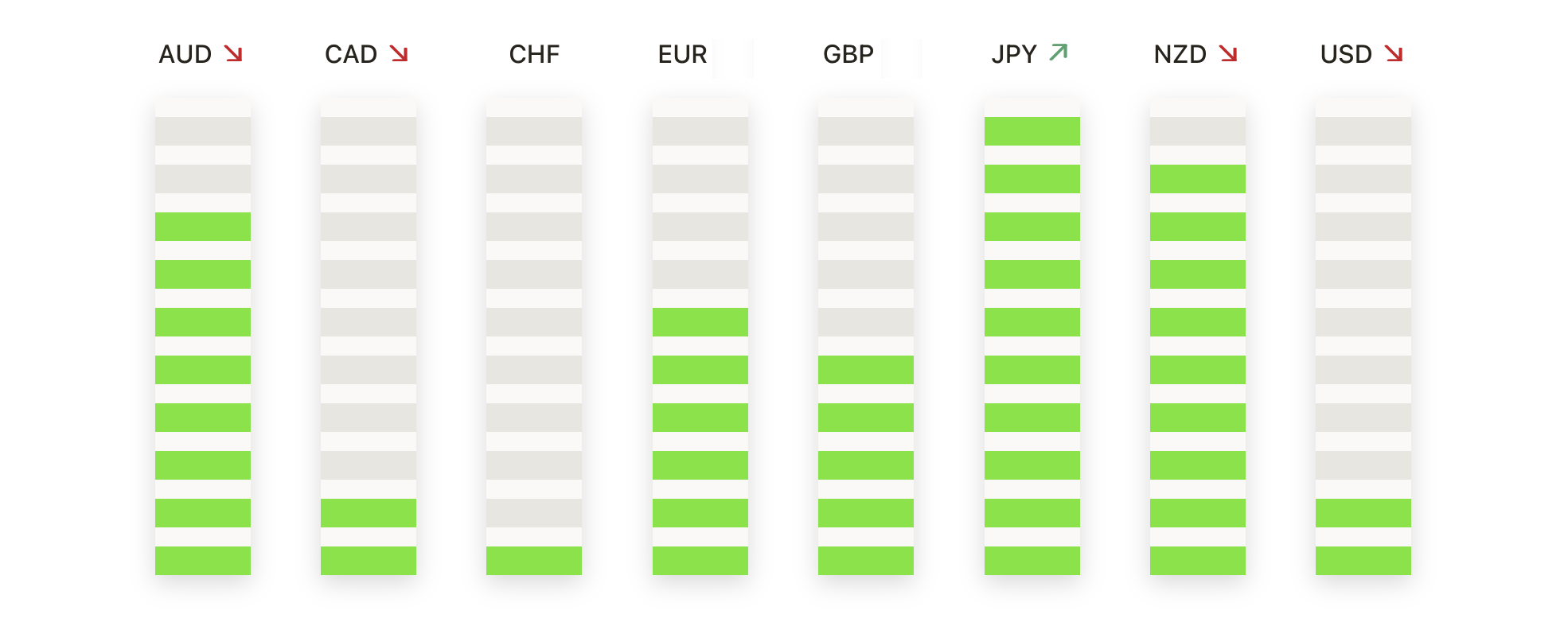

FX Today:

- EUR/USD Slips as Dollar Strengthens Ahead of Inflation Data: The EUR/USD pair fell back to the 1.1040 region on Monday as the US Dollar gained strength, driven by rising US Treasury yields and anticipation of key inflation reports later this week. The pair remains under pressure as markets await the Federal Reserve’s next move. Immediate support is seen at 1.1026, with a break lower potentially testing the 200-day SMA at 1.0997. On the upside, resistance stands at 1.1155, followed by 1.1190 and 1.1201. Traders are cautious, positioning themselves for potential volatility as US inflation figures are released.

- GBP/USD Struggles as Treasury Yields Weigh on Pound: The British Pound weakened on Monday, closing at 1.3074, down 0.43% as rising US Treasury yields put pressure on the pair. GBP/USD traded below its 100-period SMA, signalling a bearish outlook. Support is currently at 1.3040, with further downside targets at 1.3000 and 1.2960-1.2970 if selling pressure intensifies. On the upside, resistance is expected at 1.3100, with a potential rebound towards 1.3130 and 1.3150 should market sentiment shift.

- EUR/GBP Trades Sideways as Bearish Momentum Flatlines: The EUR/GBP pair closed mildly lower at 0.8440 on Monday, as the pair consolidates in a tight range. Technical indicators suggest flattening bearish momentum, with the RSI hovering around 43 and the MACD showing little directional bias. The pair is finding support at 0.8410, while resistance remains at 0.8450. If the pair breaks out of this range, it could head towards the next support at 0.8380 or the next resistance at 0.8460. Volumes have been decreasing, suggesting the market is awaiting a catalyst for further movement.

- US Dollar Gains Momentum as Inflation Data Comes into Focus: The US Dollar started the week strong, with the Dollar Index (DXY) continuing its upward trend on Monday. With US Treasury yields inching higher and traders anticipating inflation data, the greenback has gained momentum. The 2-year yield rose 3 basis points to 3.681%, and the 10-year yield held at 3.706%, supporting the Dollar’s strength. Resistance for the DXY is seen at 101.80, with further targets at 102.00 and 102.30, while downside support lies at 101.30 and 101.15.

- USD/CAD Stalls as Rising Oil Prices Cap Gains: The USD/CAD pair traded around 1.3560 on Monday, struggling to break above the strong resistance at 1.3588 (200-day moving average), as rising oil prices offered support to the Canadian Dollar. US crude oil futures rose more than 1% on Monday, which helped to limit the pair’s upside. A break above 1.3588 would expose the 1.3600 level, while further upside could test 1.3618. On the downside, support is seen at 1.3550, with 1.3500 as the next target if the pair moves lower.

- Gold Holds as Traders Await Key Inflation Data: Gold prices maintained their position above $2,500 on Monday, closing at $2,516 after hitting an intraday high of $2,523. Traders are keeping a close watch on this week’s US inflation data, which could influence Federal Reserve policy and push gold prices higher. The next major target for gold is the year-to-date high of $2,531, with further resistance at $2,550 and the psychological $2,600 mark. On the downside, support lies at $2,500, with a potential drop testing the $2,470 level.

Market Movers:

- Palantir Surges on S&P 500 Inclusion: Palantir Technologies jumped 14% on Monday after it was announced that the stock will join the S&P 500 later this month. The stock is now trading at its highest level since early 2021, benefiting from renewed investor interest. Palantir will replace American Airlines in the index, as part of the latest rebalancing. With a market cap exceeding $76 billion, Palantir has solidified its spot in the benchmark.

- Dell Gains on Long-Term Hopes: Dell Technologies rose 3.8% on Monday, following news that it will also join the S&P 500, replacing Etsy. The stock received a boost as index-tracking funds adjusted their portfolios ahead of the September 23 inclusion date. Investors remain optimistic about Dell’s long-term prospects, especially in its server and data storage businesses.

- JetBlue Rises After Analyst Upgrade: JetBlue Airways saw its stock soar 7.2% after Bank of America upgraded the airline to “neutral” from “underperform.” The analyst cited signs of improvement in the company’s revenue strategies, which are expected to contribute to a stronger financial performance. The price target was raised to $6, implying a potential 13% upside from Friday’s close.

- Summit Therapeutics Rockets on Positive Drug Trial Results: Shares of Summit Therapeutics skyrocketed 56% on Monday after the company reported that its lung cancer drug candidate outperformed Merck’s Keytruda in a phase three clinical trial. Merck, in contrast, saw its shares dip 2% on the news, as the market reacted to Summit’s promising trial data.

- Boeing Gains From Union Agreement: Boeing shares rose 3.1% after the company reached a deal with its factory workers union, potentially avoiding a costly strike. The resolution of labour disputes is seen as a major win for Boeing, reducing the risk of production delays and boosting investor confidence in the company’s operations.

- MarineMax Climbs Upon Analyst Upgrade: MarineMax, a leading boat dealer, gained 4.1% after Citigroup upgraded the stock to “buy” from “neutral.” The firm pointed to a potential boost in sales if the Federal Reserve cuts interest rates, which would lower financing costs for boat buyers. This upgrade adds to the company’s recent momentum in the recreational boating market.

- United States Steel Rises 5% on JPMorgan Upgrade: United States Steel saw its shares increase by 5% after JPMorgan upgraded the stock to “overweight” from “neutral.” The firm pointed out that the recent pullback presents a buying opportunity, and that the stock could see further upside if its planned sale to Nippon Steel proceeds as expected.

As markets kicked off the week, investor sentiment turned positive, with the Dow rebounding nearly 500 points after last week’s sharp declines, driven by optimism over a potential Federal Reserve rate cut. The S&P 500 and Nasdaq also broke their losing streaks, lifted by a broad-based rally across sectors. European stocks followed suit, posting gains across major indices, while Asian markets remained mixed, with China’s economic data continuing to weigh on sentiment. Oil prices rebounded over 1%, offering some relief after their worst week since 2023, while Treasury yields held steady ahead of key inflation data. As investors look toward critical inflation reports later this week, the market remains focused on how the Federal Reserve’s next move will impact the broader economic outlook.